Guide to financing your education

As you read this, over 9 lakh students are sweating over their Class XII examination in India.

Come April, there will be a scramble for college admissions. Considering the rising cost of higher education, most parents and students will be desperately juggling their finances. According to a calculator on cost of education provided by Aviva India, a leading insurance player, the cost of a medical, engineering or fashion designing degree in India is Rs 7-10 lakh. An MBA degree's cost starts at around Rs 5 lakh, but is Rs 15-25 lakh at the better Indian B-schools. If you want a foreign degree, be prepared to shell out double or even quadruple these costs.

Come April, there will be a scramble for college admissions. Considering the rising cost of higher education, most parents and students will be desperately juggling their finances. According to a calculator on cost of education provided by Aviva India, a leading insurance player, the cost of a medical, engineering or fashion designing degree in India is Rs 7-10 lakh. An MBA degree's cost starts at around Rs 5 lakh, but is Rs 15-25 lakh at the better Indian B-schools. If you want a foreign degree, be prepared to shell out double or even quadruple these costs.

The ideal solution would be free funding, say, scholarships. However, the competition is fierce and many students fall back on what they think is the next best free-money option: parents. Not too long ago, an Assocham survey revealed that 65% of Indian parents spend over half their yearly income on their child's education. How fair is it to wipe out a parent's retirement kitty in pursuit of the good life?

Thanks to the recent reforms and initiatives, it has never been easier to finance one's own education. For instance, under the revised model education loan scheme designed by the Indian Banks' Association, merit students taking admission in recognised private institutions under the management quota will also be eligible for study loans.

In addition, the scope of the courses eligible for education loans from banks has been widened to include degrees/diplomas in nursing. Little wonder then that banks' education loan portfolio has gone up from Rs 42,300 crore in December 2010 to Rs 52,100 crore in 2012, a jump of 23%. It also helps that the Reserve Bank of India (RBI) recently warned banks to not reject education loan applications just because a borrower does not fall under its service area.

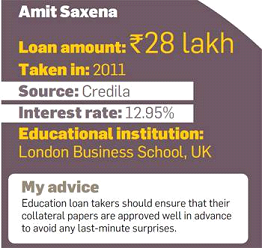

A more significant factor fuelling this growth is the increasing availability of the product. Earlier, only public-sector banks offered it in deference to the government diktat. Over time, however, private players have joined the fray and, of late, two non-banking financial companies (NBFCs) have also taken the plunge. Credila Financial Services commenced operations in 2008, and with HDFC's backing after 2009, it has emerged as the largest private-sector education loan provider in India. More recently, Dewan Housing Finance has entered this space with Avanse Financial Services.

As a result of the increasing competition, loan seekers can now avail of better interest rates, higher loan amounts and a faster, hassle-free process. Typical education loan interest rates currently range between 11.5% and 14%, compared with 15-24% for personal loans and 13-15% for loans against securities. So, if you are convinced and want to take the responsibility for your own future, go through this ready reckoner on loans.

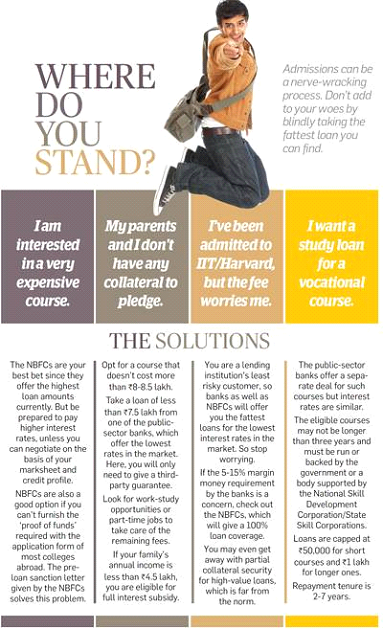

The list of eligible expenses comprises the tuition fee for approved courses, including examination and library fee. The other main categories are:

- Hostel fees.

- Travel expenses or passage money for overseas education.

- Purchase of books and relevant equipment, including a computer, at reasonable costs.

- Expenses for project work or study tours. This is, however, typically limited to about 20% of the total tuition fee payable. The public-sector banks also offer a separate deal for vocational education and training.

Eligibility criteria

According to the model education loan scheme, the two broadest eligibility

criteria are that the student must be an Indian national, and that he should have secured admission in an approved professional or technical course through an entrance test or selection process. In addition, some banks tack on the age criterion—the student should be 16-35 years old—or specify the minimum marks required in the last qualifying exam.

criteria are that the student must be an Indian national, and that he should have secured admission in an approved professional or technical course through an entrance test or selection process. In addition, some banks tack on the age criterion—the student should be 16-35 years old—or specify the minimum marks required in the last qualifying exam.

Given that most banks have a margin money requirement of up to 5% of the loan for studying in India and 15% for foreign courses (for loans above Rs 4 lakh), the applicants who are unable to drum up this amount are automatically rejected. For the record, margin money is the amount that the applicant needs to put up as down payment. Don't forget to ask the lending institution whether a scholarship can be treated as margin money.

Last, but not the least, remember that an earning parent, spouse, or guardian has to typically stand in as a co-applicant for the education loan.

Along with the completed loan application form, borrowers need to furnish proof of identity and residence, bank account statements and copies of income tax returns, marksheets of SSC, HSC and degree courses, as well as proof of admission and the fee schedule. In addition, you have to attach a copy of the scholarship letter and collateral documents, if applicable.

Source : Economic Times